11:52 JST, April 4, 2023

Gas prices are expected to jolt upward, threatening to add fresh uncertainty to the economy and increase the cost of summer travel, after Saudi Arabia and other major oil exporters significantly slashed production on Monday, ignoring demands from the White House.

The pullback by the oil-producing bloc known as OPEC Plus was framed as a “precautionary measure” to ensure stability of the energy market and came despite earlier signals that it would make no further reductions this year. As a result, several top investment banks predicted that crude prices could again hit $100 a barrel.

Rising oil prices could complicate efforts by the U.S. Federal Reserve and other central banks to get inflation under control, analysts said. Higher fuel prices – diesel in particular – would weigh on consumers’ pocketbooks and jack up costs for the shipping networks that underpin global supply chains.

That makes the OPEC Plus production cut “kind of a stick in the eye” to global economies struggling to reduce inflation without triggering a recession, said Patrick de Haan, head of petroleum analysis at GasBuddy.

Analysts are divided on how much the move might drive up gas prices, which now average $3.50 per gallon in the United States, according to AAA. The fresh cut of 1.16 million barrels per day suggests that OPEC Plus is expecting demand to weaken as summer approaches and some large economies teeter on the brink of recession. If so, prices at the pump could rise as little as 10 cents per gallon, analysts said. But if demand picks up, Americans could once again be paying more than $4 a gallon later this year.

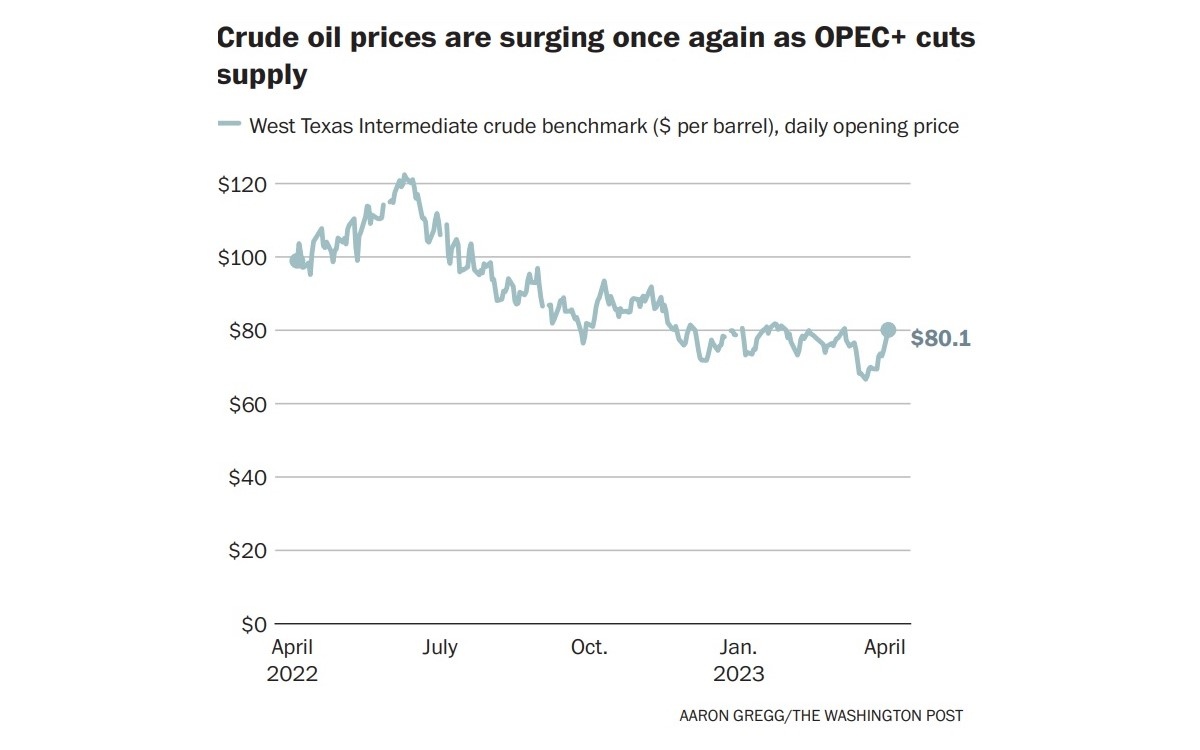

The wild card in such forecasts is China, where fuel consumption is rising as the country emerges from coronavirus lockdowns. If demand there continues to rise, some analysts caution, it could propel Brent crude, the global benchmark, back to $100 a barrel. It was trading near $85 on Monday, reflecting a nearly 6.2 percent jump following the OPEC Plus news. West Texas Intermediate crude, the U.S. benchmark, jumped 6.3 percent, above $80.

Energy stocks also got a bump, with Chevron climbing 4.2 percent; ExxonMobil, 5.9 percent; and Marathon Oil, 9.9 percent. The major U.S. stock indexes, meanwhile, were mostly higher, with the Dow Jones industrial average closing up 327 points, or nearly 1 percent, and the S&P 500 advancing 0.4 percent. The tech-heavy Nasdaq shed nearly 0.3 percent.

Regardless of the ultimate impact on prices, the move by OPEC Plus is certain to have geopolitical fallout. It was driven by Saudi Arabia, the dominant oil producer in the organization and a nation that has increasingly distanced itself from the United States, as it forges new and strengthened alliances with some of America’s longtime rivals. An October production cut of 2 billion barrels per day by OPEC Plus drew a sharp rebuke from the White House, which was anxious about the prospect of higher pump prices just weeks before the midterm election.

Though an autumn price surge never materialized – vindicating OPEC Plus’s claims that it was responding to softening demand and not aiming to interfere in U.S. elections – any cuts by the organization in this period of global energy instability are generally viewed as hostile in Washington. The latest cut could revive conversations on Capitol Hill about retaliatory legislation that would expose OPEC Plus to antitrust lawsuits when it hikes prices, and push the White House to rekindle its efforts to intervene in energy markets.

The tools at Washington’s disposal are few, however. Last year, the administration tapped more than 180 million barrels from the nation’s Strategic Petroleum Reserve in an effort to stabilize prices, leaving limited opportunity to drain more. In fact, the White House is under pressure to buy oil to refill the reserve.

Any new drilling permits the administration grants will not have a meaningful immediate effect on the world’s oil supply, as it takes time to bring new operations into production. Calls to impose “windfall taxes” on large oil companies have yet to gain strong bipartisan support in Congress, amid worries that such taxes will backfire and lead oil producers to reduce their investment in infrastructure and move more of their operations abroad.

One state that has acted against fuel producers, California, is taking a cautious approach. Gov. Gavin Newsom backed off his push for a windfall tax on oil companies after failing to get enough traction in the legislature. He instead signed into law last month a novel but modest measure through which state regulators will track profit margins at refineries, with power to impose fines if those profits are deemed excessive.

OPEC’s move closely follows an announcement by Russia to cut oil output by 500,000 barrels a day beginning in March.

The cost of crude soared last year after Russia invaded Ukraine, upending global energy markets. Prices hit $130 a barrel last fall before cooling off, and gathered close to $70 per barrel this year as weakness in the banking sector raised fears of a possible recession.

Analysts believe the production cuts could force energy prices up once again. Three investment banks ― Raymond James, Pickering Energy Partners and Goldman Sachs ― predicted they will add $10 or more to the price of a barrel.

“OPEC+ has very significant pricing power relative to the past, and today’s surprise cut is consistent with their new doctrine to act preemptively because they can without significant losses in market share,” Goldman wrote in a note to clients. Goldman analysts said the decision to cut production may have been driven in part by the continued release of millions of barrels of oil from the U.S. strategic reserve, which kept prices down, and the refusal of the Biden administration to start buying oil to refill it.

Goldman projects Brent crude will hit $95 a barrel by the end of this year. Others believe oil prices could nudge even higher: CMC Markets analyst Tina Teng told CNBC that oil might be headed “toward the $100 mark again,” given the long-awaited reopening of China’s economy after years of harsh coronavirus restrictions.

De Haan, the GasBuddy analyst, says U.S. fuel prices could go from $3.60 to $3.85 a gallon, on average, if oil prices stay above $90 a barrel. Gas prices tend to lag crude by several weeks, meaning hikes at the pump wouldn’t materialize until late April. That would still reflect an improvement for U.S. motorists, who on average were paying $4.19 per gallon a year ago.

De Haan said prices could drop again if a recession crimps U.S. demand, noting that demand has been “sluggish” in the first few months of 2023.

“Oil markets were taken aback by this decision,” De Haan said of Monday’s move, “but don’t be surprised if some of this fizzles.”

Gasoline demand, measured as a four-week moving average, stood at 8.76 million barrels a day as of March 24, up just 0.6 percent from a year ago, according to the U.S. Energy Information Administration.

“It’s hard to tell what exactly this will do to inflation . . . I don’t see this as a game changer yet, because the economy is still continuing to struggle,” De Haan said.

Oil industry experts cautioned against putting too much stock in any forecast of where prices will land this summer given the various economic and geopolitical factors that could send demand swinging in one direction or the other. Among the big wild cards is Saudi Arabia’s next move.

“The Saudi oil market strategy since President Biden took office has been consistently less predictable and less favorable to U.S. interests,” said an email from Jim Krane, an energy research fellow at Rice University’s Baker Institute for Public Policy.

“Unfortunately, this means Americans are exposed to greater oil market risk because the Strategic Petroleum Reserve remains underfilled.”

Most Read

Popular articles in the past 24 hours

-

‘Dry Bonsai’ Gives New Life to Withered Trees, Allows Free Artist...

-

Japanese Students Use Traditional Pickle to Create Novel Wagashi ...

-

McDonald's Japan Raises Prices; Big Mac to Cost ¥500, Double Chee...

-

Nepal Bus Crash Kills 19 People, Injures 25 Including One Japanes...

-

Japan’s Nikkei Stock Average Rises as AI-Related Stocks Shine; Co...

-

Astellas Collaborates with Vir to Develop Its Experimental Prosta...

-

Early-Blooming Kawazu Cherry Blossoms Create Sea of Pink at Park ...

-

Joruri Bunraku Narrative Performed in Honor of Donald Keene by La...

Popular articles in the past week

-

Producer Behind Pop Group XG Arrested for Cocaine Possession

-

Japan PM Takaichi’s Cabinet Resigns en Masse

-

Sanae Takaichi Elected Prime Minister of Japan; Keeps All Cabinet...

-

Japan's Govt to Submit Road Map for Growth Strategy in March, PM ...

-

Bus Carrying 40 Passengers Catches Fire on Chuo Expressway; All E...

-

U.S. Firm to Build Training Hub in Fukushima N-plant for Debris R...

-

Japan, U.S. Name 3 Inaugural Investment Projects; Reached Agreeme...

-

Riku-Ryu Pair Wins Gold Medal: Their Strong Bond Leads to Major C...

Popular articles in the past month

-

Producer Behind Pop Group XG Arrested for Cocaine Possession

-

Japan PM Takaichi’s Cabinet Resigns en Masse

-

Japan Institute to Use Domestic Commercial Optical Lattice Clock ...

-

Man Infected with Measles Reportedly Dined at Restaurant in Tokyo...

-

Israeli Ambassador to Japan Speaks about Japan’s Role in the Reco...

-

Videos Plagiarized, Reposted with False Subtitles Claiming ‘Ryuky...

-

Man Infected with Measles May Have Come in Contact with Many Peop...

-

Prudential Life Insurance Plans to Fully Compensate for Damages C...

Top Articles in News Services

-

Survey Shows False Election Info Perceived as True

-

Hong Kong Ex-Publisher Jimmy Lai’s Sentence Raises International Outcry as China Defends It

-

Japan’s Nikkei Stock Average Touches 58,000 as Yen, Jgbs Rally on Election Fallout (UPDATE 1)

-

Japan’s Nikkei Stock Average Falls as US-Iran Tensions Unsettle Investors (UPDATE 1)

-

Trump Names Former Federal Reserve Governor Warsh as the Next Fed Chair, Replacing Powell

JN ACCESS RANKING

-

Producer Behind Pop Group XG Arrested for Cocaine Possession

-

Japan PM Takaichi’s Cabinet Resigns en Masse

-

Japan Institute to Use Domestic Commercial Optical Lattice Clock to Set Japan Standard Time

-

Man Infected with Measles Reportedly Dined at Restaurant in Tokyo Station

-

Israeli Ambassador to Japan Speaks about Japan’s Role in the Reconstruction of Gaza