To use this site, please disable the ad blocking feature and reload the page.

This website uses cookies to collect information about your visit for purposes such as showing you personalized ads and content, and analyzing our website traffic. By clicking “Accept all,” you will allow the use of these cookies.

Users accessing this site from EEA countries and UK are unable to view this site without your consent. We apologize for any inconvenience caused.

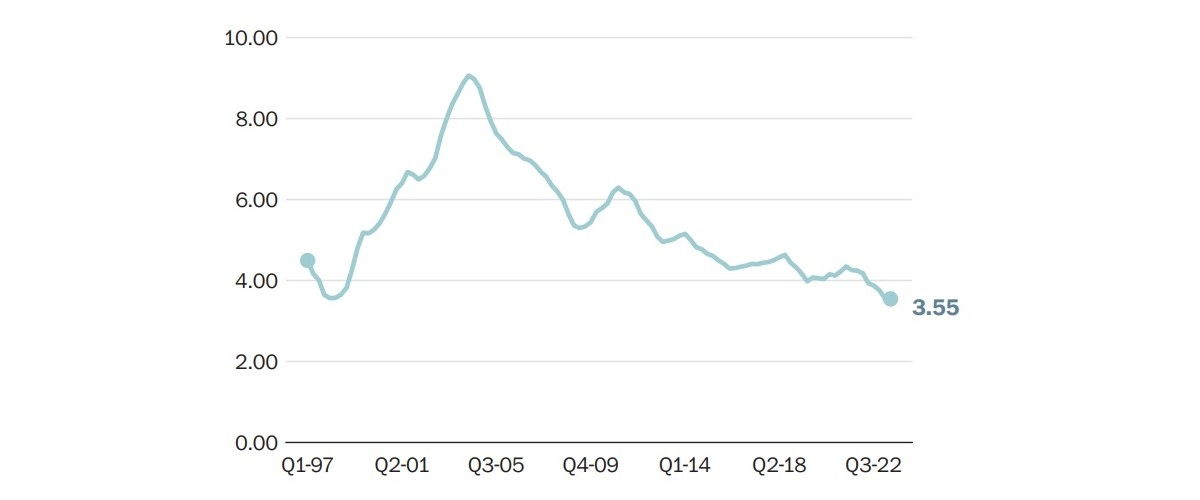

DAVID J. LYNCH / THE WASHINGTON POST China’s demand for foreign manufactured goods has been declining Chinese imports of manufactured goods, excluding components used in re-exports, as a percentage of GDP; Trailing four-quarter sum Source: Calculations by economist Brad Setser with data from Haver Analytics and China’s General Administration of Customs

The Washington Post / David J. Lynch

15:15 JST, September 5, 2023

Judith Marks, the chief executive of the elevator maker Otis Worldwide, returned in April from a 10-day trip to China saying “all signals look positive” for the country’s recovery from its draconian covid lockdown.

Almost immediately, the economic outlook began to darken.

The Chinese rebound that seemed to be gaining momentum in April lost steam in May and reached midsummer in danger of petering out altogether. Suddenly, the world’s second-largest economy, for years a reliable juggernaut, was ailing. The core of the problem: a debt-ridden, overbuilt property sector that threatened to smother growth well short of the government’s 5 percent annual target.

Chinese weakness is bad news for companies such as Otis, based in Farmington, Conn. China is its most profitable market for new equipment sales, accounting last year for roughly one-third of orders. Through the first half of the year, China was the company’s only major market where orders were in decline.

But the elevators that Otis sells in China are made there. So while the property market slump means that fewer are needed, most of the pain will be felt at Otis facilities in China, not in the United States. For all its remarkable progress and prosperity, China is not an important enough customer of goods produced elsewhere for its woes to be contagious. At least for now.

“China has been less of a growth engine than is widely assumed,” said Brad Setser, a former Biden administration trade adviser. “The direct effects of its slowdown are going to be relatively modest. It doesn’t matter to the export side of the U.S. economy if China grows at zero or China grows at 5 percent.”

That could change if China’s slowdown proves worse than anticipated, unnerving global financial markets, or if the government artificially cheapens its currency in a bid to export its way out of the crisis at the expense of its trading partners.

But China’s downshifting economy is likely to clip just a few tenths of a percentage point off global growth, economists have said. One indication of the country’s modest impact can be seen in its trade in manufactured goods, such as industrial equipment, automobiles, furniture and appliances.

China’s imports of manufactured items for its own use, rather than to make products for customers in other countries, amount to just 3.5 percent of gross domestic product, according to Setser. And China’s reliance on foreign factories is about one-third lower than when Xi Jinping became the country’s leader in 2012 and accelerated a self-sufficiency drive.

“That’s unusually low,” said Setser, now a senior fellow with the Council on Foreign Relations. “China makes almost all of the manufactured goods consumed in China.”

Otis, which has plants in Tianjin and near Shanghai, has operated in China since the mid-1990s. Its elevators and escalators are used in infrastructure projects, such as the Tianjin metro, as well as in the residential and commercial developments at the heart of China’s real estate bubble.

Although the property market slowdown is pinching new equipment orders, demand for servicing of installed units remains strong, Marks told investors in July, when Otis reported higher quarterly sales and earnings.

To be sure, a prolonged downturn in China – or one that is deeper than expected – would be felt around the world. First to suffer would be major commodity producers. The Chinese economic miracle for decades has vacuumed up copper from Peru, ore from Australia, soybeans from Brazil and oil from Saudi Arabia and Russia.

Direct financial links between the United States and China have thinned in recent years, amid a trade war and rising geopolitical tensions. But a deeper Chinese slump could set off a “negative feedback loop,” with sinking stock and bond prices, rising volatility and a soaring dollar combining to sap consumer and business confidence in the United States and elsewhere.

Such a scenario, akin to the fallout from the 2015 Chinese stock market crash, could shave half a percentage point off global growth and 0.3 points off U.S. growth, according to Gregory Daco, the chief economist at EY-Parthenon.

“What matters to the U.S. and the rest of the world is if the China shock is translated into a broad-based deterioration in overall financial conditions,” he said.

China’s neighbors are already feeling a chill. But their decline in exports to China is primarily the result of American consumers buying fewer electronics than they did during the work-from-home phase of the pandemic rather than a consequence of Chinese domestic weakness.

China sits at the center of a pan-Asian electronics supply chain, assembling products with components shipped there from South Korea, Malaysia, Thailand and Taiwan.

Multinational corporations that serve the domestic Chinese market also would be hurt. The German automaker BMW depends on China for more than 29 percent of its annual revenue. More than 27 percent of Intel’s sales come from Chinese customers.

“China does matter for the global economy. Germany is a big exporter to it. It matters for commodity markets. It sets the tone for emerging Asia,” said Nathan Sheets, the global chief economist at Citigroup.

But China’s old growth model, which relied on heavy investment in public infrastructure and housing, is exhausted. After decades of frenzied growth, the country has just about all the high-speed rail lines and apartment complexes that it needs.

Chinese leaders have said they intend to pivot to an economy based on more consumer spending and service industries. But “there’s still a long way to go,” Sheets said.

The current slowdown underscores a shift in China’s global image. For years, China’s vast domestic market beckoned multinational corporations with the promise of enormous profits. And it seemed certain to surpass the United States as the world’s largest economy.

Now, the outlook is less rosy. China grew in the second quarter at an annual pace just above 3 percent, a far cry from the roughly 9 percent rate it averaged over its first three decades of economic reform. Its aging labor force is shrinking, and Xi emphasizes loyalty to the Communist Party rather than expanding the economy.

Visiting Beijing last week, Commerce Secretary Gina Raimondo said U.S. business executives have told her that China is “uninvestable” because of the government’s increasingly erratic treatment of foreign businesses.

“China is growing slower and building less. It’s not going to be uniquely central the way it used to be,” said Scott Kennedy, a senior adviser at the Center for Strategic and International Studies (CSIS).

The International Monetary Fund says China will contribute more than one-third of global growth this year. But that figure overstates China’s impact on its trading partners, some economists have said. Rather, it demonstrates the arithmetic truth that China, even with all its problems, is a large economy that will grow faster than its counterparts. That produces a large output gain, but most of the benefits stay at home.

China runs a sizable trade surplus with the rest of the world, meaning it sells to other countries much more than it buys from them. Chinese exporters dominate global markets for products such as electronics, footwear and aluminum, while consumers in China save much of their income rather than spending it on foreign goods.

As the Federal Reserve and other major central banks tried to cool inflation by raising interest rates over the past year, foreign demand for Chinese goods sagged. Through July, Chinese exports were down 5 percent from the same period in 2022. But imports fell nearly 8 percent, meaning the surplus widened.

“Countries that run a trade surplus basically subtract more from global growth than they contribute,” said George Magnus, an economist at Oxford University’s China Center. “It’s doing more for its own growth than it’s contributing.”

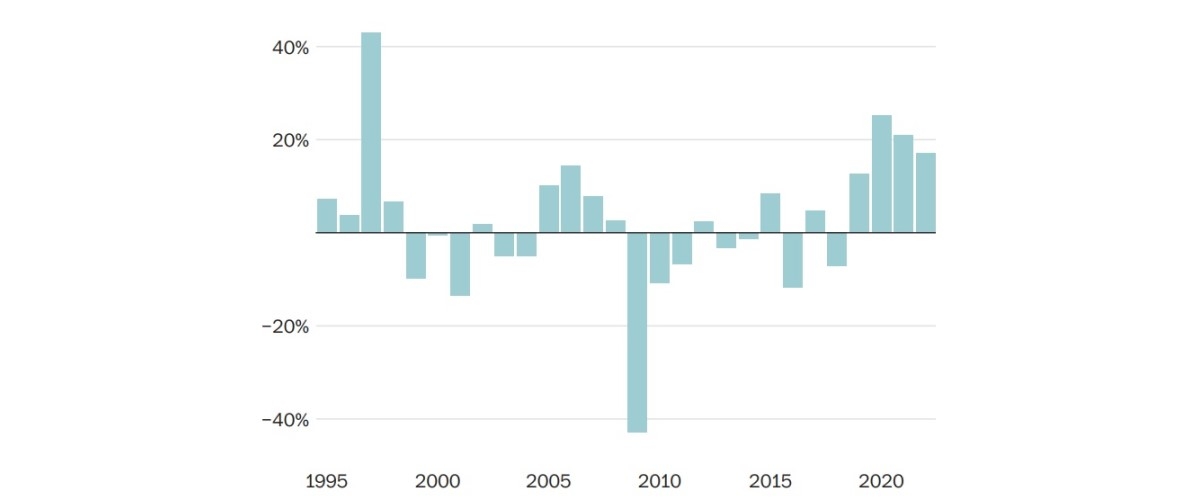

DAVID J. LYNCH / THE WASHINGTON POST Share of China’s annual economic growth from net exports Source: ChinaPower Project at the Center for Strategic and International Studies

Exports have been a central ingredient in China’s economic strategy for decades. Government officials have repeatedly spoken of promoting domestic consumption. But in the past three years, China’s export sector has delivered more than one-fifth of the country’s annual economic growth, the largest share since the 1997 Asian financial crisis, according to the ChinaPower project at CSIS.

China began the year with hopes for a boom. In December, Xi reluctantly relaxed his strict zero-covid policy after rare public protests. Freed from lockdown, Chinese consumers were expected to drive an economic rebound.

But after a burst of spending, the recovery fizzled. Fresh government data showed Chinese factories, consumers and real estate developers all mired in a slump.

“They’re structurally in a deep hole that they’re going to have a lot of difficulty climbing out of,” said Andrew Collier, the managing director of Orient Capital Research in Hong Kong.

Chinese authorities have taken a number of steps to revive growth, including cutting interest rates. But they have made little headway. And with more than 21 percent of young people unemployed, the prospect of social unrest looms.

One lever Beijing has not pulled is manipulating the value of its currency.

The yuan this year has fallen 5 percent against the dollar, reflecting China’s slower growth and lower interest rates. The government could further cheapen the yuan by selling it on global markets. That would effectively discount Chinese goods, making them less expensive for customers paying with dollars and euros.

Swamping foreign markets with made-in-China products would raise export earnings and boost domestic employment. But it would be certain to worsen already fractious relations with the United States and Europe.

There’s no sign yet that the Chinese authorities plan to make such a move. But if the economic deterioration accelerates, they might.

After all, they have done so before. China kept its currency undervalued for years after joining the global trading system in 2001, prompting years of complaints from the U.S. government and American businesses.