To use this site, please disable the ad blocking feature and reload the page.

This website uses cookies to collect information about your visit for purposes such as showing you personalized ads and content, and analyzing our website traffic. By clicking “Accept all,” you will allow the use of these cookies.

Users accessing this site from EEA countries and UK are unable to view this site without your consent. We apologize for any inconvenience caused.

The Washington Post / Hanna Zakharenko, Abha Bhattarai, Janice Kai Chen

12:43 JST, August 1, 2023

There’s good news for renters: Your too-high rent is finally not skyrocketing anymore.

Monthly asking prices shot up by 15 percent between 2020 and 2022, marking the fastest run-up in rents in nearly a century. But now costs are calming down.

Rent growth around the country is back at pre-pandemic norms – growing about 1 to 3 percent per year, according to real estate data firm CoStar Group. In some recent hot spots, including Austin and Atlanta, prices are actually falling.

“The rental market is finally taking a breath,” said Igor Popov, chief economist at Apartment List. “This summer looks a lot different from the last two summers: We are getting to a more stable period, and in some parts of the country, renters are back in the driver’s seat.”

Overall, year-over-year asking rents rose 1.1 percent as of June 30, down from 2.8 percent in March, CoStar data shows.

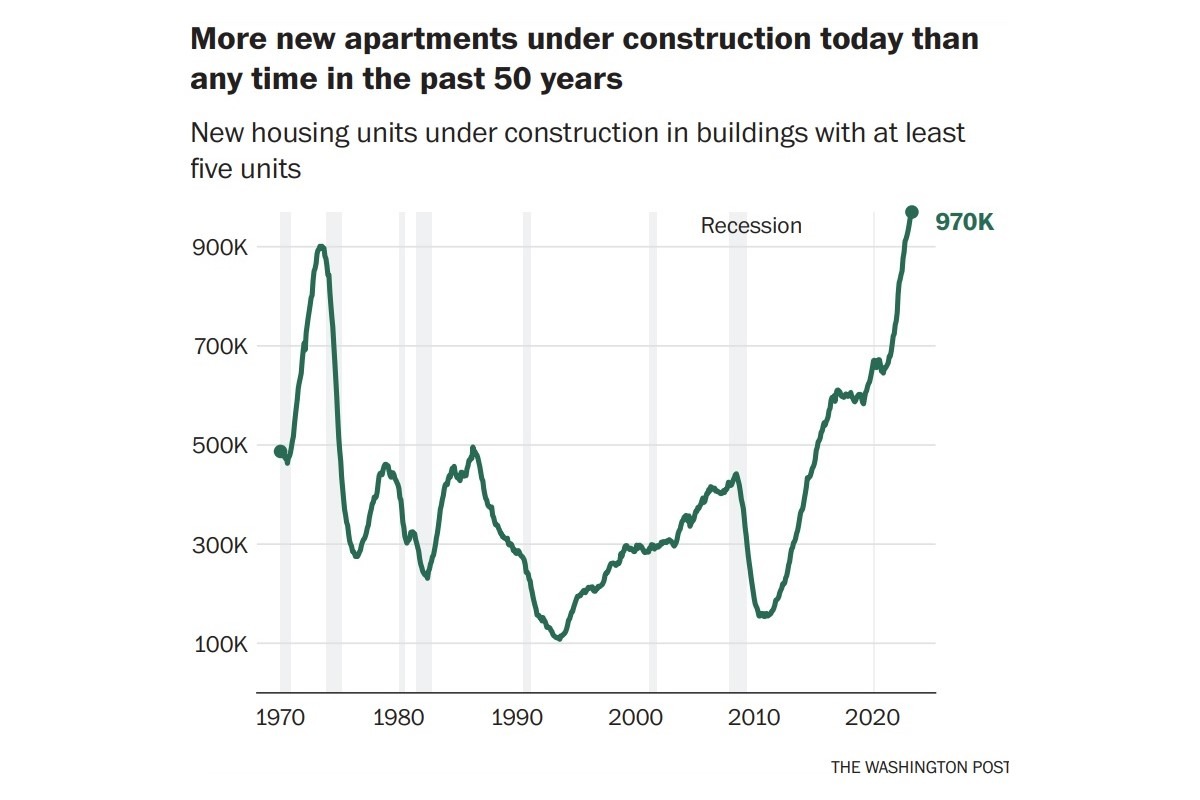

The biggest reason for that slowdown: more housing. Nearly 1 million new apartment units – an all-time high – are under construction around the country, census data shows. Of those, 520,000 are expected to hit the market this year, with another 460,0000 to follow in 2024, according to CoStar.

At the same time, appetite for rentals is declining as Americans settle into post-pandemic living and spending patterns. Demand for apartments plummeted in 2022, falling to the weakest level since 2009, according to RealPage Market Analysis. Although rental activity has rebounded somewhat since, it is still markedly lower than it has been. Fewer people with roommates are branching out on their own. Young adults are staying put in their parents’ homes. And retirees who might’ve downsized from homeownership to rentals are waiting for the housing market to pick back up before relocating.

The result is a growing mismatch between available apartments and potential renters, which is tamping down price growth.

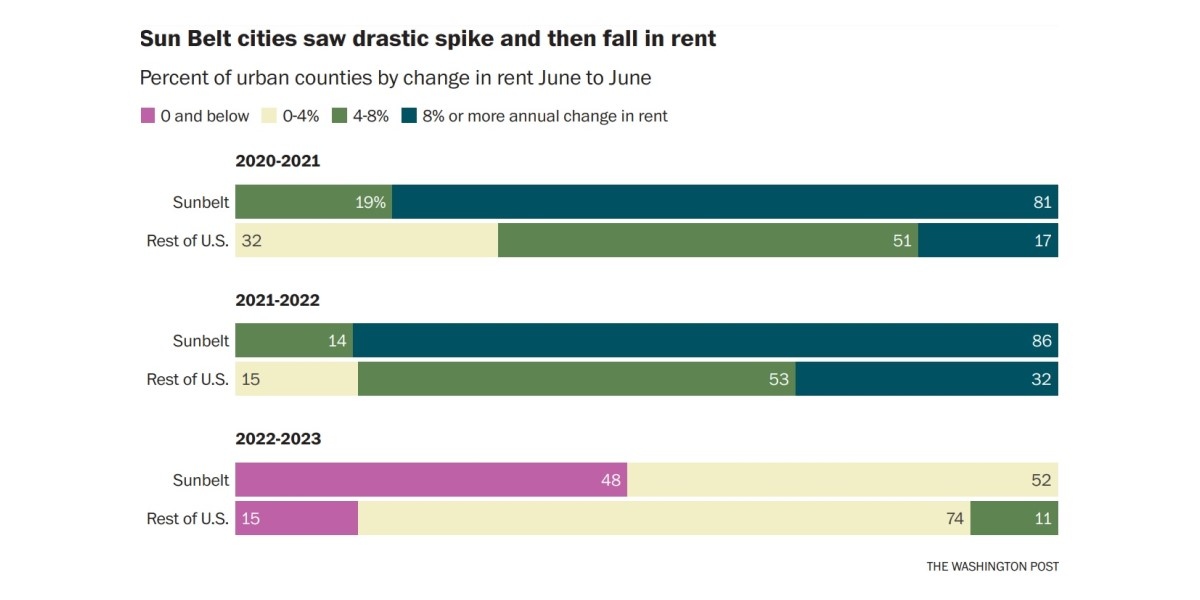

That’s especially the case in the Sun Belt, where developers have rushed to cash in on growing demand for rentals. An influx of new residents early in the pandemic – mostly white-collar workers leaving urban centers like New York and San Francisco in search of warmer weather and cheaper housing – led to a sudden rental boom in many Southern cities. Annual rents in Phoenix, Dallas and Miami rose as much as 16 percent between 2021 and 2022, CoStar data shows.

But now rent increases have come to a standstill – and are expected to drop even further – as new options inundate the market. In many areas of the Sun Belt region, such as Las Vegas, Austin and Nashville, prices have dropped 1 to 3 percent in the past year, according to CoStar.

“We’ve seen a surge of apartment units in the Sun Belt, and that’s because of the big bounce those states had early in the pandemic,” said Jay Lybik, national director of multifamily analytics at CoStar. “Developers accelerated their plans to add units in those locations, and that’s what is coming online now.”

The Washington Post

The majority of those new rentals – 70 percent of them, he said – are in luxury properties, with amenities such as rooftop swimming pools, co-working spaces and spas, meant to cater to recent transplants with large budgets.

But with demand cooling, those luxury apartments are also seeing the biggest price declines. Rents for high-end apartments have fallen 0.2 percent in the past year, while prices for mid- and lower-tier properties have risen by as much as 3 percent in the same period.

“We’re finally getting the supply that was built in response to the pandemic demand boom,” said Daryl Fairweather, chief economist at Redfin. “That stock is finally here – and for higher-income renters, that means there’s a whole new buffet of options.”

Still, rents are considerably higher than they were in 2019 and unlikely to go back to pre-pandemic levels, even in the most volatile markets, according to experts.

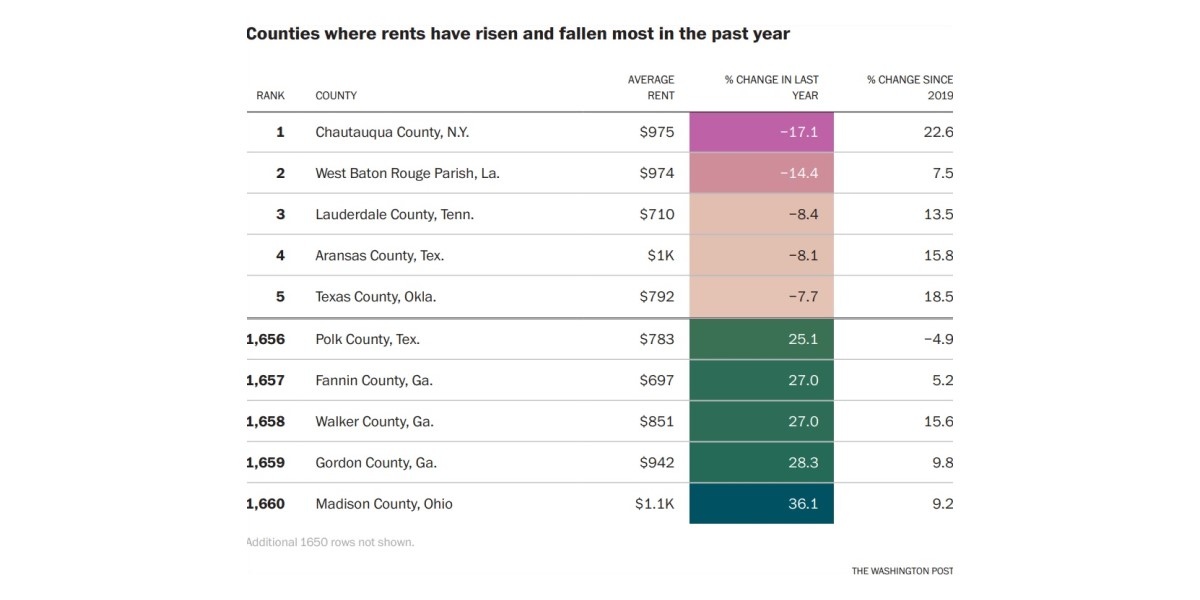

In the Atlanta area, for example, rents rose 23 percent between 2019 and 2022. And although monthly costs have recently started to decline – by 2 percent, so far this year, to an average $1,648 – renters are paying about $330 more each month than they were before the pandemic.

Overall demand in the Atlanta area is steadily declining: More people moved out of apartments than into them in the first half of 2023, according to broker Oleg Konstantinovsky. Meanwhile, the market has added 7,000 new apartment units so far this year, he said, with another 50,000 under construction.

Many new buildings, he said, are offering perks, such as one or two months of free rent. That’s putting pressure on existing apartment complexes to keep rents steady – and is driving down overall price growth.

“Incentives are definitely coming back. People are getting a little bit of cost savings,” he said. But, he added, “although Atlanta is certainly not as affordable as it used to be.”