To use this site, please disable the ad blocking feature and reload the page.

This website uses cookies to collect information about your visit for purposes such as showing you personalized ads and content, and analyzing our website traffic. By clicking “Accept all,” you will allow the use of these cookies.

Users accessing this site from EEA countries and UK are unable to view this site without your consent. We apologize for any inconvenience caused.

Photo by Scott Suchman for The Washington Post. Businesses and households, which are already struggling to deal with soaring prices, say looming economic uncertainty has made it difficult to make long-term plans.

The Washington Post/Abha Bhattarai

14:03 JST, July 29, 2022

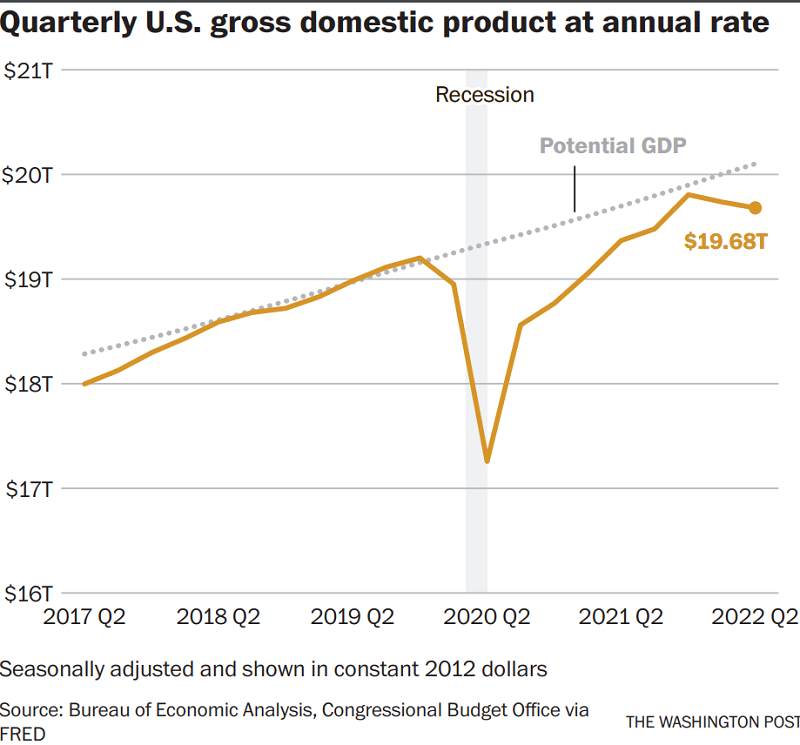

The U.S. economy has shrunk for a second straight quarter, at an annual rate of 0.9%, raising concerns that the country may be heading into a recession and compounding the Biden administration’s political challenges as it grapples with decades-high inflation.

The new figures, released Thursday by the Bureau of Economic Analysis, come at a tumultuous time for the economy, though economists disagree on the likelihood of a full-fledged slump. In the past, six months of contraction have usually indicated a recession. The official determination is made by a panel of experts, though recessions aren’t typical when unemployment is near record lows.

The second-quarter slowdown reflected shifting consumer and business behaviors. Retailers bought fewer items, including cars, as consumers shifted their spending away from goods to services such as restaurants and hotels. Declines in home construction and government spending also contributed to the negative reading.

The sour report on the gross domestic product reflects ongoing problems with inflation, which has been at 40-year highs for several months, as well as weakening home sales and challenges for some corporate sectors, including tech and finance. Even the red-hot labor market is beginning to show cracks. Broader worries about the war in Ukraine, the global financial outlook and aggressive interest rate increases have prompted many economists to predict a recession in the next year.

“Broadly, this shows an economy that is really slowing,” said Jason Furman, an economics professor at Harvard University who was a top economic adviser to President Barack Obama. “This data is much more worrisome than it was in the first quarter. I don’t think you can easily dismiss these numbers. It isn’t just volatile factors anymore. Meaningful, important parts of the economy are slowing.”

The White House has pushed back hard against suggestions the economy is in a recession, with senior officials, including Treasury Secretary Janet Yellen, pointing to a strong labor market as a sign that the recovery remains on track. Before Thursday’s report, White House officials had argued that even a negative growth figure for the second quarter shouldn’t be seen as a sign that a recession had arrived.

“Coming off of last year’s historic economic growth . . . it’s no surprise that the economy is slowing down as the Federal Reserve acts to bring down inflation,” President Joe Biden said in a statement Thursday. Later speaking to reporters, Biden ticked off a litany of high points for the economy, including jobs creation, low unemployment and business investments, ending with: “That doesn’t sound like a recession to me.”

Republican lawmakers have blamed the Biden administration’s stimulus spending for contributing to inflation and the broader economic contraction, with many claiming the country is in a recession.

Photo by: The Washington Post — The Washington Post

“You don’t need a fancy economics degree to have seen this coming,” Rep. Kevin Hern of Oklahoma said in a statement Thursday. “Biden’s spending over the last 18 months is directly responsible for the economic situation we’re in today.”

The U.S. economy unexpectedly slowed by an annual rate of 1.6% in the first three months of the year, largely because of a mismatch in trade – with the United States importing far more than it was exporting – and a drop in inventory purchases by businesses that were still flush with leftover goods from the holidays.

In many respects, the economy is in uncharted territory. The only time there have been six months of contraction without a recession appears to have been in 1947, according to Tara Sinclair, an economics professor at George Washington University.

Some of the signs of a slowdown in economic growth are by design, thanks to interest rate increases aimed at cooling down the economy. The Federal Reserve again raised interest rates on Wednesday, this time by three-quarters of a percentage point – an unusually aggressive increase – in hopes of curbing inflation, which hit 9.1% in June, compared with the year before.

The Fed’s interest rate increases, which began in March, are already beginning to cool demand in certain parts of the economy. On Wednesday, Fed Chair Jerome Powell pointed to a number of data points – including slower growth in consumer spending, weakening demand for housing and lower business investments – as signs that the central bank’s efforts are working.

But, he added, it’s getting tougher to calm the economy without sending it into a tailspin.

“Our goal is to bring inflation down and have a so-called soft landing, by which I mean a landing that doesn’t require a significant increase in unemployment,” Powell said in a Wednesday news conference. “We understand that’s going to be quite challenging. It’s gotten more challenging in recent months.”

Still, most economists expect the U.S. economy to end the year with growth – albeit at a much slower pace than the 5.7% gain it notched last year. Lydia Boussour, lead U.S. economist at Oxford Economics, for example, expects economic growth to slow to 1.9% this year and 1.1% in 2023.

“We are expecting the economy to slow quite sharply,” she said. “The key question is: What happens in the second half of the year, and where does that leave the economy?”

The GDP report showed that Americans are spending less on goods, particularly on items such as food, beverages and household supplies. However, spending on services, such as travel and dining out, rose modestly in the second quarter.

Businesses and households, which are already struggling to deal with soaring prices, say looming economic uncertainty has made it difficult to make long-term plans. Some families are putting off big-ticket purchases, while employers say they are rethinking hiring plans and bracing for a broader pullback in spending.

Walmart this week slashed its profit expectations for the year, causing its stock price to drop nearly 9%. The country’s largest retailer, considered a bellwether for the industry, said it will have to mark down products more heavily than expected because higher gas and grocery costs are forcing many consumers to rethink buying patterns.

General Motors, meanwhile, reported a 40% drop in quarterly profits and announced plans to curb hiring. Other major employers – including Ford Motor, 7-Eleven and Shopify – are going even further, announcing hundreds, even thousands, of layoffs.

However, the labor market is not showing the same signals of deterioration as the rest of the economy and does not indicate that the country is in a recession, despite signs of a slowdown. The unemployment rate remains at a steady 3.6% and job creation is strong, signaling that workers still maintain leverage in a hot labor market.

“When it comes to the labor market, it’s definitely sending different signals than what GDP numbers are suggesting,” said Nick Bunker, economist research director at Indeed. “Demand for workers is strong. Hiring intentions are high.”

There are still some strong signs that suggest the job market is edging closer to a downturn. Unemployment claims been trending up in recent weeks, payroll growth is slowing and tech companies have significantly pulled back on hiring.

Listings for software developer jobs have fallen 17% in the last four weeks, according to jobs site Indeed. Tech hubs such as San Jose, San Francisco and Seattle have all seen a drop-off in job postings over the same period, Indeed data shows.

Meanwhile, tech giants such as Apple and Facebook parent company Meta are pausing hiring, with employees at the latter bracing for job cuts as high as 10%. These companies could be responding to a decrease in consumer demands and a sense of uncertainty about whether they’ll be able to support their current workforce if a recession comes.

“I take all these signals pretty seriously,” said Guy Berger, principal economist at LinkedIn. “I’m not quite at the stage where I want to call these things recessionary. But it’s quite conceivable that the labor market will be headed toward a mild recession as we move through the year.”

Those job losses, or just the looming fear of one, could lead Americans to tighten their belts, which would further slow the economy.

Amanda Meadows, a comic book editor in Los Angeles, was unexpectedly laid off this month. She isn’t fretting yet – her partner still has a good-paying job in the video game industry and she’s hopeful she can find work soon – but that hasn’t stopped her from rethinking her spending habits.

“All the frivolous stuff – my restaurant budget, my clothing budget, my books budget – all of those have been cut down significantly,” said Meadows, 36. “If the money is better left in savings, that’s what we’re doing.”

Mark Beneke, who owns a used-car dealership in Fresno, Calif., is starting to see worrisome signs in the economy: Demand for cars is beginning to slow, and auto loan delinquencies and repossessions are on the rise.

But he says he isn’t panicking yet. Beneke is still hiring, though he says he may cut back on his marketing budget and start buying fewer cars – perhaps 12 a week instead of 15 – if the slump continues.

“We’re being cautious, but we’re not necessarily scared to the point where we’re freezing,” said Beneke, of Westland Auto Sales. “Things don’t seem overly concerning yet.”

On Thursday, Yellen disputed GOP claims that the economy is in a recession, saying that it showed signs of continued expansion in consumption and reflected a welcome change from growth that was too fast.

“Overall, with a slowdown in private demand, this report indicates an economy transitioning to more steady, sustainable growth,” Yellen said, adding that recessions are typically defined by economists to include “substantial job losses and mass layoffs,” business closures, a decline in private-sector activities, and a “broad-based” weakening of the economy.