To use this site, please disable the ad blocking feature and reload the page.

This website uses cookies to collect information about your visit for purposes such as showing you personalized ads and content, and analyzing our website traffic. By clicking “Accept all,” you will allow the use of these cookies.

Users accessing this site from EEA countries and UK are unable to view this site without your consent. We apologize for any inconvenience caused.

The Yomiuri Shimbun A screen displays Japan’s Nikkei stock average, which temporarily surged to the 39,400 level, on Tuesday morning in Chuo Ward, Tokyo.

By Daisuke Ichikawa / Yomiuri Shimbun Staff Writer

10:54 JST, February 27, 2024 (updated at 16:00 JST)

Japanese and U.S. stock markets continue to hit all-time highs. In the long term, U.S. stock prices have risen more than 10-fold, while the Nikkei Stock Average on the Tokyo Stock Exchange has remained weak. The recent rise in Japanese stock prices is due mainly to foreign investment and the depreciation of the yen. In order for Japan to achieve substantial growth, it is essential to create a “virtuous cycle,” in which vigorous domestic investment supports the growth of Japanese companies.

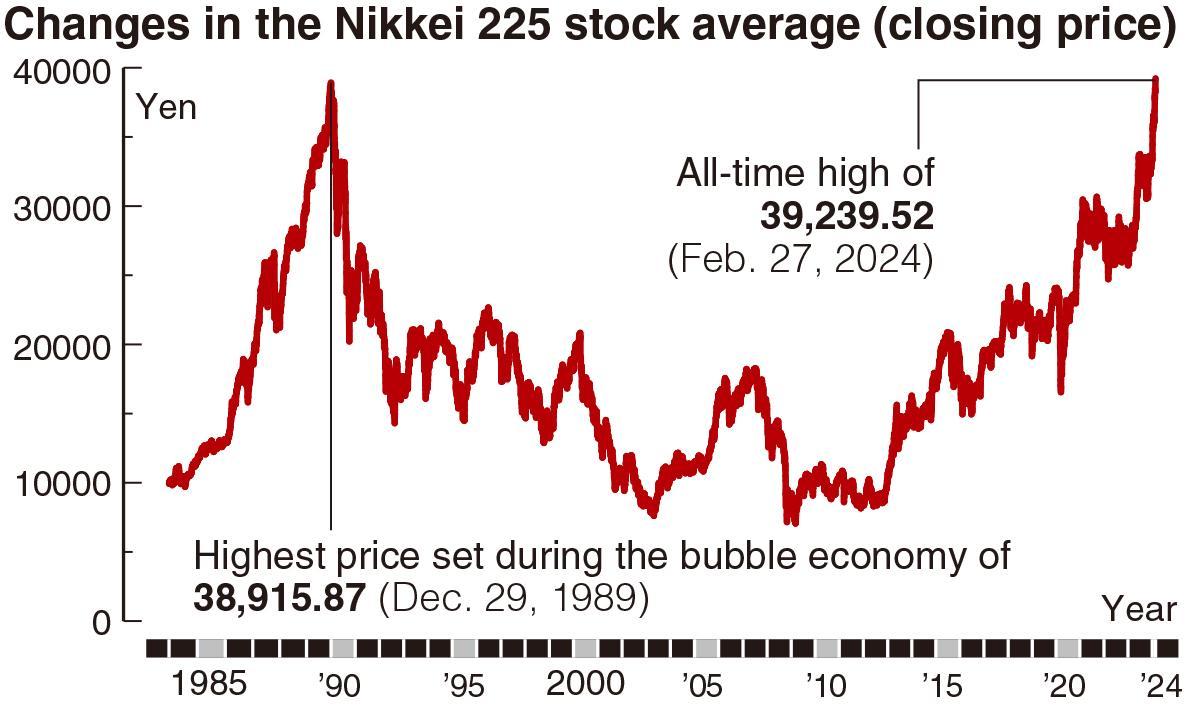

35 times higher than 1989

The Nikkei 225 stock average set an all-time closing high for the first time in 34 years and two months, breaking the previous record of 38,915.87 set on Dec. 29, 1989. Meanwhile, the U.S. Dow Jones Industrial Average has risen nearly 14-fold from 2,753 at the end of 1989, and the tech-focused Nasdaq Composite has increased about 35-fold over the same period.

Regarding the decades-long slump in Japanese stock prices, Satoshi Osanai, senior economist at the Daiwa Institute of Research, Ltd., said, “In the United States, many technological innovations have occurred, and information technology giants that emerged in that process have earned profits in the global market.” According to the Internal Affairs and Communications Ministry, when the private IT investment volume in 1995 is expressed as an index of 100, volume in Japan for 2021 was 191, slightly less than twice that of 1995. Yet volume in the United States over the same period increased nearly 15-fold to 1,487.

Because of this, U.S. IT giants such as Microsoft Corp. and Apple Inc. dominate the global market today. In 1989, seven Japanese companies including Nippon Telegraph and Telephone Corp. and an urban bank were among the world’s 10 largest companies by market value.

U.S. semiconductor company Nvidia Corp. was founded in 1993 and is currently the world’s fourth largest company by market capitalization, a representation of the rapid growth of high-tech companies’ stocks. On the other hand, when it comes to Japan, Toyota Motor Corp. ranks 24th, the highest place among Japanese companies. Toyota’s total market value — about 300 billion dollars — is nearly one eighth that of Microsoft.

Deflation

In 1989, Japan experienced and economic bubble, and many Japanese stocks were overvalued compared to their actual performance and the state of the economy. When the bubble burst in 1991, sky-high stock and land prices plunged, and the Japanese economy entered the “Lost 30 Years” of economic stagnation. Companies reduced investment and wage hikes, while consumers tried to cut back on spending. As a result, Japan entered a vicious cycle of deflation where the prices of goods and services fell.

After the launch of the second Cabinet of former Prime Minister Shinzo Abe in December 2012, a large amount of capital was injected into the market under the government’s aggressive fiscal policy and the Bank of Japan’s large-scale monetary easing policy. The Japanese stock market finally began to recover.

Hiromi Yamaji, chief executive officer of Japan Exchange Group, Inc., expressed his expectations on Monday: “Japan seems to be getting out of deflation.”

The Yomiuri Shimbun

‘Productivity is key’

The main cause of the recent surge in stock prices is foreign investment in Japanese companies that have transformed themselves with better performance and corporate governance since the end of last year. In addition, the global generative artificial intelligence boom has helped increase the stock prices of semiconductor-related companies. Japanese stocks also look undervalued due to the depreciation of the yen. Meanwhile, the slowdown of the Chinese economy has caused foreign investors to move their money out of China and into the Japanese market. Japanese companies need to keep changing in order to attract more investors at home and abroad.

Izuru Kato of Totan Research Co. said, “In the United States, the economy is expected to continue to grow against the background of population growth, which encourages investors to invest in the country. In order for Japanese companies to enhance their earning power, increasing productivity through such strategies as talent development is key.”